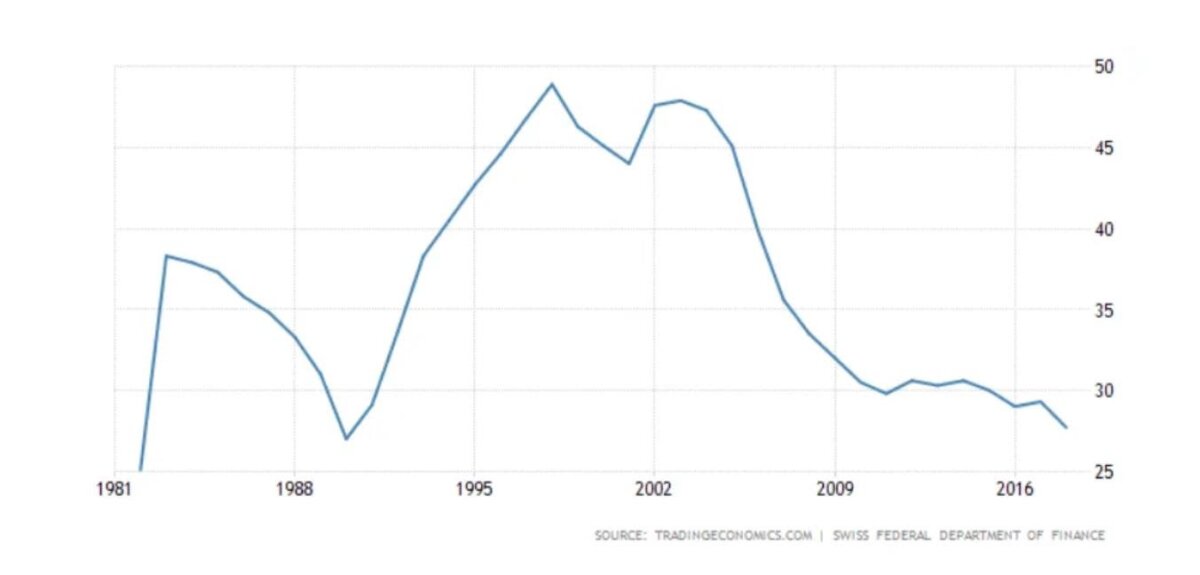

Switzerland Government debt-to-GDP ratio, 1980 – 2020

- Low level financial risk: Many Swiss banks such as Zurcher Kantonal Bank, Postfinance, etc. have a state guarantee for the total account balance of up to 100,000 CHF. This means that the state of Switzerland itself guarantees that your money will be secure up to this amount even if the bank fails for some reason. Other banks such as UBS and Credit Suisse are so big that they can sustain their financial positions even in times of crisis.

- Elite level of privacy: Swiss banks’ reputation is based on trust, so they can cooperate with tax and criminal investigations – but even today, Swiss banks give a level of privacy unavailable anywhere else in the world.

How to choose a proper Swiss bank

In Switzerland, banks are loosely divided into several groups:

- The Premier League: First of all, these are top-level banks such as UBS, Credit Suisse and Julius Bär. These three banks actually dominate the market in terms of volume, number of employees, relationships with institutional groups, etc. They also have an international presence.

- Middle League: Next is the Middle League, or League Two. These are smaller banks that are incorporated in Switzerland, but do not have many international branches. These banks include such institutions such as Banque Bonhôte & Cie SA, J. Safra Sarasin, Migros Bank, Zurich Cantonal Bank, etc.

- Boutique banks: Then there are very small, privately-owned banks, such as Mirabaud, Swissquote, WIR Bank, etc. These banks provide very personal services to a small number of very rich clients.

As a rule, in the premier league, banks have the most severe requirements for the selection of customers. Naturally, what they offer depends on the situation in the market, but each bank has a so-called minimum amount of liquidity that needs to be in the account. And this volume in the first major league banks is usually the highest.

Citizens of Russia and the CIS for example. Usually they need to maintain at least 100 million euros. Although we know of exceptional cases – sometimes as low as 10-15 million euros – most elite bankers generally don’t accept deposits of less than 50 million euros.

In terms of secrecy, Swiss law forbids the banks from disclosing any information regarding an account or even of its existence, without the client’s permission. So as far as secrecy goes, there is no difference between a large bank such as UBS and any one of the smaller banks.

Some Swiss banks promote secrecy as a selling point – that they offer more privacy to their account holders, than banks anywhere else, but Nikolaev says this can lead to misconceptions.

And although Swiss bank accounts are world-leading for privacy and confidentiality, they will always make sure their customers are genuine and they certainly won’t turn a blind eye to criminality:

Оften small banks portray a scenario that if God forbid, something bad happens to you in your own country, then a request from the prosecutor’s office or from the court from your country will most likely arrive in the big banks of Switzerland, and since they are too small, and unknown to most of the world, no one will send them a request for information about your account. And if there is no request, then they don’t have to give any information to anyone. This is partly true. However, if we are talking about the request of information with tax authorities at a government level, then it does not matter what size the bank is.

Kirill Nikolaev

What do Swiss banks look for, before approving an account?

Broadly speaking, there are two types of client looking to open a Swiss bank account. The first lives outside of Switzerland. The second lives in Switzerland. Banks treat these cases individually.

For non-Swiss residents, these are the two main areas that the bank will carefully analyse. Banks want to get a solid understanding of both, before they approve or refuse your bank account application.

- The first is the background profile of the bank account applicant

- The second is about the capital to be deposited and maintained in the bank

Essentially, the bank will be looking to verify the public identity of the applicant and proof of his legal and financial eligibility.

They will look for information available about you in the public domain. So before applying, make sure there are no negative publications or references that might influence their decision. Have you ever been involved in any public scandals or legal proceedings? Because if you have, a Swiss bank may well consider that a red flag, and refuse the application.

They will be making sure, during basic, first-level screening, that they are not dealing with criminal or politically blacklisted citizens. These may be current officials or former officials in governments, their agencies, or other positions of public office. Citizens under sanctions in certain countries can also be refused.

If the individual himself is directly involved in some kind of criminal or political activity or officially being investigated, then it is practically impossible to open a Swiss bank account. Even if some time has passed and he was a former government functionary, then most likely the bank will refuse.

The second issue is what we call the origin of capital. And here, the first thing the bank asks for is to explain the origin of the capital and then confirm it with authentic documents. Previously, about 20-25 years ago, this was merely a formality, but now this is taken very seriously.

According to Nikolaev, the new law changes were important and have improved the banking system, unlike the previous era where no questions were asked:

Some Swiss bankers recall with nostalgia the times when customers came with a suitcase of money, in cash, and bankers, looking into their eyes, asked, ‘Where did this money come from?’ They answered something and it suited them. No one asked unnecessary questions.

Now they are asking for documents that explain the origin of capital. And they probe deeply to confirm all claims. They also expect notarized documents from any country the documents originate.

So, if you sold an apartment, received an inheritance, or traded assets in the stock markets, they will ask for a whole bunch of documents. Where did you get these assets from? How long did you own these assets? And many other legitimate questions too. They all need to be certified by the relevant authorities, even if they are influential current or former politicians, says, Nikolaev:

The former president of a post-Soviet country asked to become a client of our family office. However, we were forced to refuse, because, first of all, at that moment, he was in the field of view of law enforcement agencies and was under a potential criminal investigation. It makes no sense to take in the client if the origin of his capital cannot be explained at all.

What the banks are looking for is to ensure that the client is absolutely transparent. He is never implicated in any negative publicity and there are no legal proceedings against him. They want to be certain he is not a criminal and that he is absolutely clean. There should be no track record of any wrongdoing.

Once it is clear the client is clean, the bank evaluates how much they can earn from that client. The bank earns money from commissions, from opening an account and from operations of an account.

Most banks do not like customers who just want to transfer 10 million euros and let the money lie in situ. Otherwise, the bank earns only a basic interest. Banks make money from commissions on investments.

That is often why banks choose to close an account. Because money lying dormant in an account does not earn any significant money. They are looking for dynamic sales and corresponding commissions for the bank. So they want to activate the maximum range of services they provide. Swiss banks look to approve clients that utilise their full suite of financial services.

How to increase your chance of getting your account approved?

The Swiss are proudly cosmopolitan, but should the applicant be a tax-paying resident of Switzerland, more harmonious relations with the bank are likely.

Banks always look at which jurisdiction the client resides but law-abiding residents of any nation may be accepted. In any case, the basic requirements for opening a Swiss bank account remain, but clients who obtain tax and residency status in Switzerland typically gain preferred status.

Can a bank change its mind and close an account?

Yes. A bank can review the client’s status at any time and can close an account if deemed necessary.

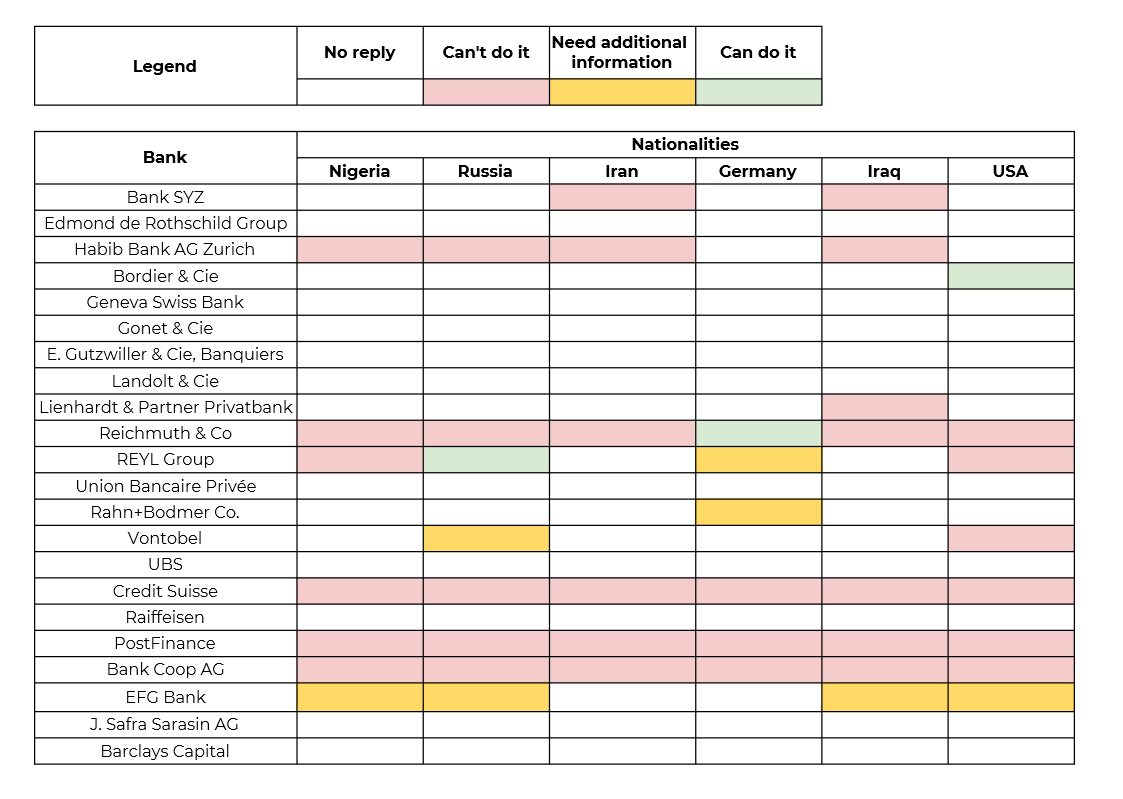

What nationalities can open an account?

Restrictions on nationalities vary from bank to bank and depend on the current political situation. For example, litigation by the US Department of Justice against UBS and Credit Suisse, has led to more stringent requirements for US citizens that want to open a Swiss bank account.

Swiss banks were accused of helping US citizens to avoid or reduce taxes that they had to pay the United States. It resulted in a huge fine for Swiss banks. And, of course, the financial crisis of 2008, had serious consequences. So legislators in the European Union and Switzerland worked to improve regulations to prevent illegal financial transactions on the continent too.

These regulatory changes resulted in the banks being even more careful about the type of clients they accept and also the type of assets they hold.

Does the nationality matter when opening a bank account in Switzerland?

As a little experiment, we wrote to some top banks in Switzerland and asked them if we could open an account. For this purpose, we created several emails typical of countries from our research: USA, Iran, Iraq, Germany, Russia, Nigeria.

The results of the research are presented in the following table.