Swiss residential real estate: Where are we now?

In 2022, following a swift rebound from the initial shock of the pandemic, demand for owner-occupied housing in Switzerland regrettably relapsed to subdued levels, as witnessed in 2020. This retreat can be attributed to the aftermath of Russia’s invasion of Ukraine, coupled with the notable upsurge in interest rates and inflation.

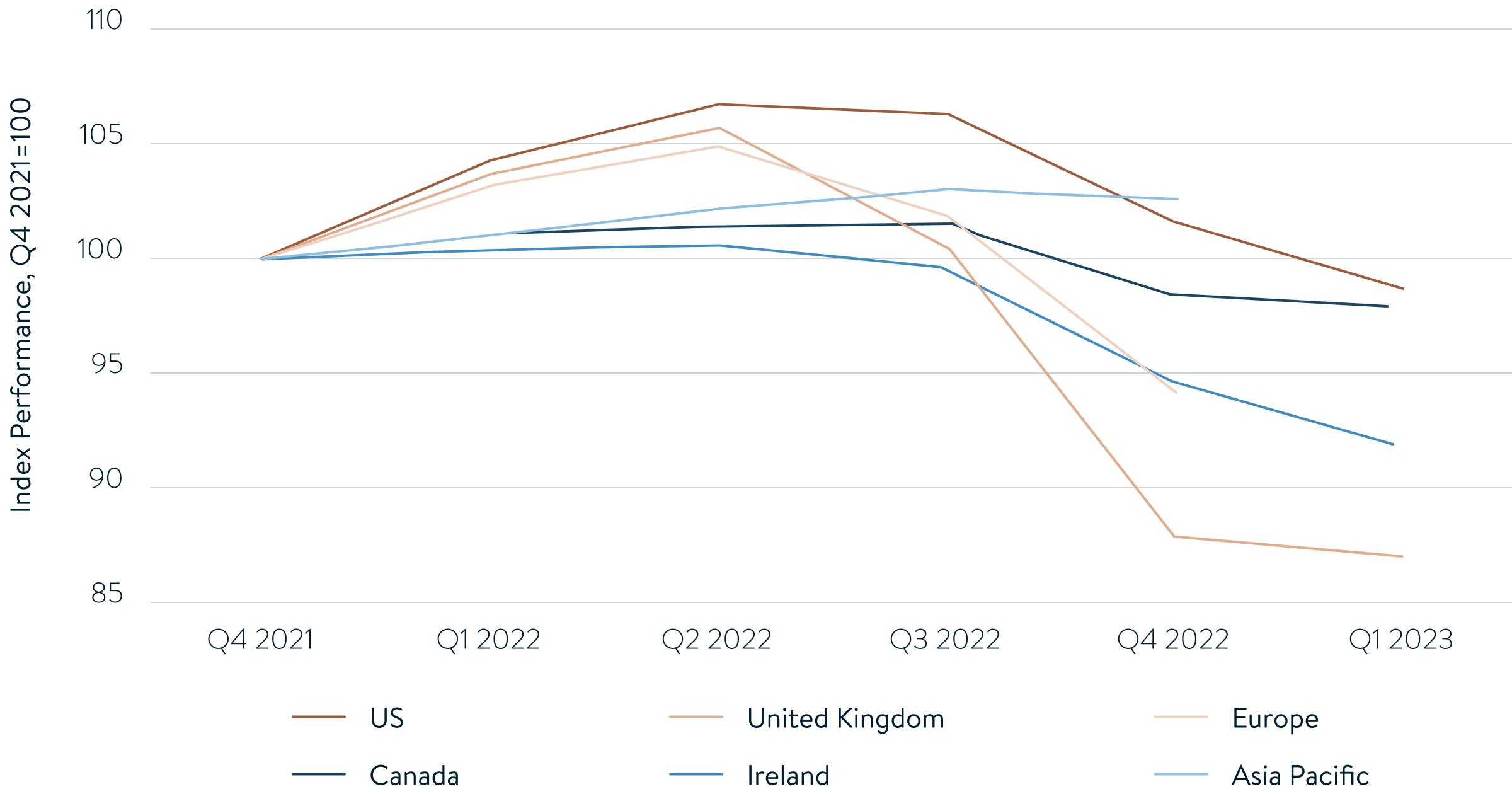

Swiss housing demand indices (last data point: December 2022)

Source: Credit Suisse

The annual interest on a five-year fixed-rate mortgage has risen from about 1% to 2.7% in just one year. While this adjustment may seem modest when juxtaposed against the historical average interest rate of 4% for similar loans over the long term, the practical impact was substantial. Essentially, it meant that in cash terms, the annual loan servicing cost for an average condominium (4.5 rooms) rocketed from CHF 8’250 to CHF 21’380.

For young adults, this was an extremely heavy additional burden, especially when almost all other costs, like fuel, food, travel, entertainment, etc. – had also surged considerably.

Food, energy, and overall prices in Switzerland (2015=100, January 2003 – July 2023)

Source: OECD

The actual values of homes, however, did not experience a sustained decline; instead, it was the rate of growth in prices that fell. Over the second quarter of 2023, for instance, average home prices increased by 1.2% but remained 2.4% higher than the year before, and an impressive 15.9% above what they were by the end of 2019.

In this context, it was affordability, rather than valuation, that was the deciding input for potential buyers in the Swiss residential real estate market, throughout 2022. This continues to be true for 2023, with Switzerland having the 9th highest house-price-to-income ratio worldwide.

The house-price-to-income ratio in selected countries worldwide (2015=100, Q2 2023 or latest available)

Source: OECD

For investors, these costs signify that the buy-to-let market is no longer attractive despite the ongoing expansion in demand. Even though, the upward movement of rental rates for homes, which can partly be attributed to the persistent growth of net immigration, could paint a different picture.

As a consequence, the yield from real estate investments now lags at less than 1.5 percentage points behind that of 10-year Swiss government bonds. This disparity is surely not enough to make high-maintenance rental properties a more appealing investment than "buy-and-forget" bonds – whether government-issued or corporate.

Given these considerations, one might expect prices to undergo a gradual and prolonged decline. The reason this has not yet come to pass, however, is predominantly due to an acute issue of scarcity in supply.