Overview of top investment options: Where to invest money in Switzerland and how to get the best return on 50K – 100K CHF for foreign and domestic capital. A professional take on the current status quo of foreign investment opportunities in Switzerland, plus an analysis of the pros and cons of the most popular investment methods by one of Switzerland’s top 5 entrepreneurs in the service sector (according to Swiss Economic Forum), Mr. Alexander Hubner, CEO of Le Bijou.

It’s not easy to be an investor. If you have earned a somewhat significant amount of money, you immediately join the elite club of people struggling with an elite disease: where can you put your wealth to grow it?

Keeping cash is probably the worst thing you can do with your wealth, second only to spending it all for nothing. The chances are, though, that not long after you’ve worn an investor’s hat, you realized that there aren’t many attractive investment options available.

See also:

- Investing 1M: Key principles, opportunities and risks overview

- Investing 200K: How to find satisfactory returns

- Investing 100K in Switzerland

The super-rich learned how to turn millions into billions and don’t need your relatively small funds. The poor can’t help either. The most fruitful deals are not yet available to you, as the entry ticket is too high, and the available options are rather disappointing. That is exactly why rich families and their offices are constantly seeking out and fighting over the best deals all over the world; some bankers travel 300 days a year looking for great investment projects.

To assist mid-sized and retail investors on their difficult path, I have put together a brief overview of investment options in Switzerland. I spent the last 11 years investing in Swiss assets and I hope this advice will help you put your money to work with more efficiency.

Quick summary (jump to section):

1. Swiss bonds

Returns: -0.8% to 0.7% (2018) for different bond types; real estate bonds yield up to 3%.

Risks: Bonds are widely considered the safest investment option.

2. Swiss stocks

Returns: Vary widely; Swiss index funds (close to “average” market returns) show between 0.37% and 1.32% annual returns.

Risks: Picking individual stocks is highly not recommended for non-professional traders.

3. Hedge funds

Returns: Vary widely, not predictable.

Risks: Highly not recommended, as the performance of most funds is worse than the average market performance over the long run.

4. Direct real estate investments in Switzerland

Returns: 2% to 4% p.a. for mid-market; 10% and higher for luxury properties

Risks: The demand can be dependent on nearby factories and offices of big companies

5. Real estate crowd-financing

Returns: 6% to 17% p.a.; best luxury properties can yield up to 20% when structured right.

Risks: The demand can be dependent on nearby factories and offices of big companies.

6. Bank deposits in Switzerland

Returns: -0.5% to 0.5% p.a.

Risks: The bank provides no collateral for investors.

7. Robo advisors

Returns: Vary widely, not predictable.

Risks: Specific to the platform and approach.

8. Wealth Management: top family & multifamily offices in Switzerland

Returns: N/A, as usually wealth management companies create custom portfolios for investors that consist of other instruments, covered or not covered in this article.

Risks: Bad management and/or wrong incentives of the manager.

9. Investing in Gold in Switzerland

Returns: N/A, as the only returns that can be made come from the changes in gold’s price, which is unpredictable.

Risks: The price is unpredictable.

Best major types of investment options in Switzerland

There currently exists quite an array of options as far as investments are concerned. The key to a successful portfolio lies in the careful and thoughtful decision making process that best fits your investment goals, keeping in mind capital, timeframe and potential risks. Below, you’ll find a breakdown of the major types of investments. Hopefully, it will be a useful tool as you create your investment strategy.

1. Investing in bonds

Returns: Vary from -0.8% to 0.7% for different bond types; real estate bonds yield up to 3%.

Risks: Bonds are widely considered as the safest investment option.

A bond is a fixed-income security, whereby an entity borrows funds from an investor for a specific time period and promises to return capital at maturity with a fixed or variable interest rate.

Characteristics of a Bond

- Bonds are usually traded by a corporate entity or a government for a project or a specific purpose.

- Bonds may be traded on exchanges or over-the-counter.

- The parties partaking in the bond investment cycle are referred to as the “Issuer” on one end, and the “Bondholder” or “Creditor” on the other.

- The main body of the bond is referred to as “Bond principal”, which is returned upon maturity date at a contractually specified “interest rate” (AKA “coupon rate” and “payment”).

- Bonds are issued at face value (e.g., $100 or 1000 CHF) that is termed “par” and the payment is calculated as per fixed interest based on par.

- Coupon Dates are the fixed dates in time whereby payment of interest is made to the Investor by the Issuer until maturity date is reached, up to 30 years. Coupon dates are usually fixed at annual or semi-annual periods.

- The Creditor has no ownership rights arising from the owning of bonds, unlike in the case of stock investments.

Advantages of bond investments

- Low risk – bonds are one of the safest and statistically low-risk investment methods.

- Bondholders’ rights are preferred over stockholders’ rights – those who own bonds get paid first.

- Readily available information for due diligence on most of the municipality and government bonds in the form of economic forecasts and ratings.

Disadvantages of Bond Investment

- Low returns that accompany the high security of bond investment.

- Brokerage and custody fees can eat out your profit, so they need to be accounted for at an early stage of decision making to provide a feasible comparison between the brokers.

Swiss bond investment

Many of the major banks will offer bond investments as part of their services portfolio. This is the time to compare the fees based on your initial investment criteria. The broker comparison tool by Moneyland.ch is invaluable for this purpose.

All major banks will trade in bonds. Here are some of the most innovative and reliable institutions for your consideration:

Swiss real estate bonds

Some companies offer real estate bonds that pay up to 3% p.a. while keeping your risk at a minimum, as your cash flow is backed by a piece of real estate.

Extra resources for Bond Investments:

- Swiss Government Bond overview by Investing.com

- Major Swiss Stock Exchange SIX Group

- Berne eXchange (BX) the second largest Swiss stock exchange

Looking to invest in bonds online? Choose your online broker with Investopedia

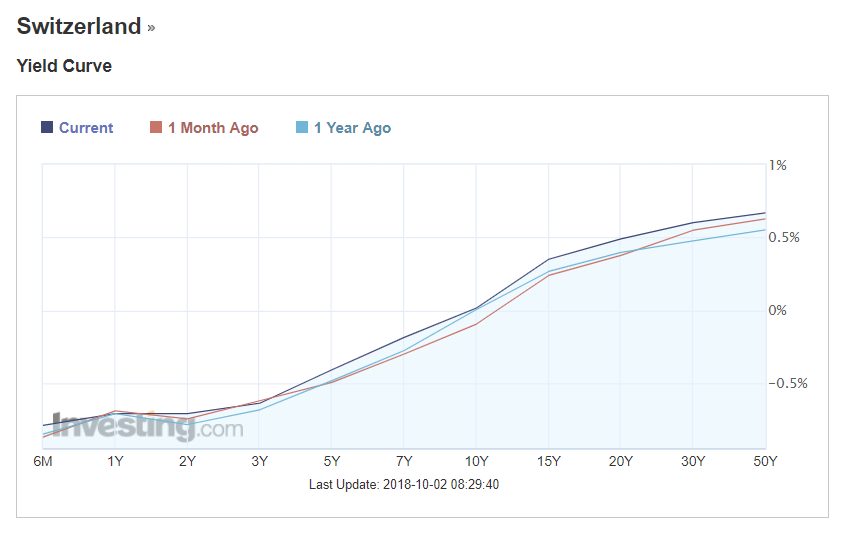

Investing in Swiss Government Bonds: Interest Rates

2. Investing in stocks

Returns: Vary widely; Swiss index funds (close to “average” market returns) show between 0.37% and 1.32% annual returns.

Risks: Picking individual stocks is highly not recommended for non-professional traders.

Stocks are a form of investment, whereby an investor gets to own a proportionate share of a company, i.e. its assets and earnings, when buying its shares (AKA stock or equity).

Characteristics of a Stock

- An investor in corporate stocks is referred to as a “shareholder”.

- Common stock allows its owner to have voting rights and dividends on the company’s earnings, as well as provides ownership rights to a share of the company.

- Preferred stock suggests that a stakeholder will not vote but will have higher dividends as well as ownership rights to a portion of a company.

- Stockbrokers are usually the licensed professionals who are eligible to buy and sell stocks on stock exchange markets.

- Stocks may be sold OTC (Over-The-Counter) as well as openly on the stock exchange with the latter being easily subjectable to due diligence and the former almost impossible to gauge from this perspective, as private companies have no obligation to disclose their financial information.

Just as with bonds, there is a primary and secondary market for stocks, primary being the shares issued to the stock exchange in the process of the IPO, when a privately-held company becomes a public one.

How to successfully trade stocks?

There’s no easy answer.

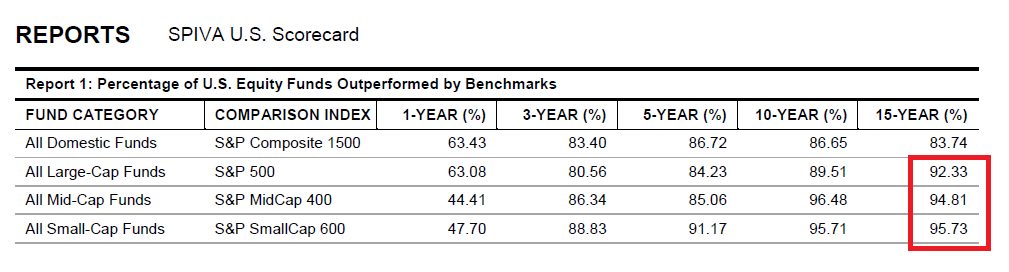

One thing you might want to consider is that most of the professional fund managers can’t beat the market (just one item of research: 95% of equity funds in the US performed worse than a distributed investment in the market, i.e. “index”). If professionals can’t beat the market by picking stocks, what evidence makes you think that you can beat it?

If you are a middle-level investor and you don’t have reasons to believe that you are the next investment genius like Ray Dalio or Warren Buffet, I’d encourage you to not to pick individual stocks but rather invest in market indices (index funds), the pro’s and con’s of which are described below.

Pros of passive stock investment in index funds

- If you invest in index funds (not in individual stocks!), you will almost always do better than you would if holding cash. If you consider the stock market in the US, there were only 4 short periods, huge crises, where you would have made more money in the long run if you had stayed in cash.

Cons of passive stock investment in index funds

- As the economy moves in cycles, after a bull market always comes a bear market, so even your investments in index funds (i.e. investments in the market overall) can temporarily lose their value.

- Potential of no returns or even losing it all if a company goes bankrupt (think Dell losing market value when not keeping up with smartphone era).

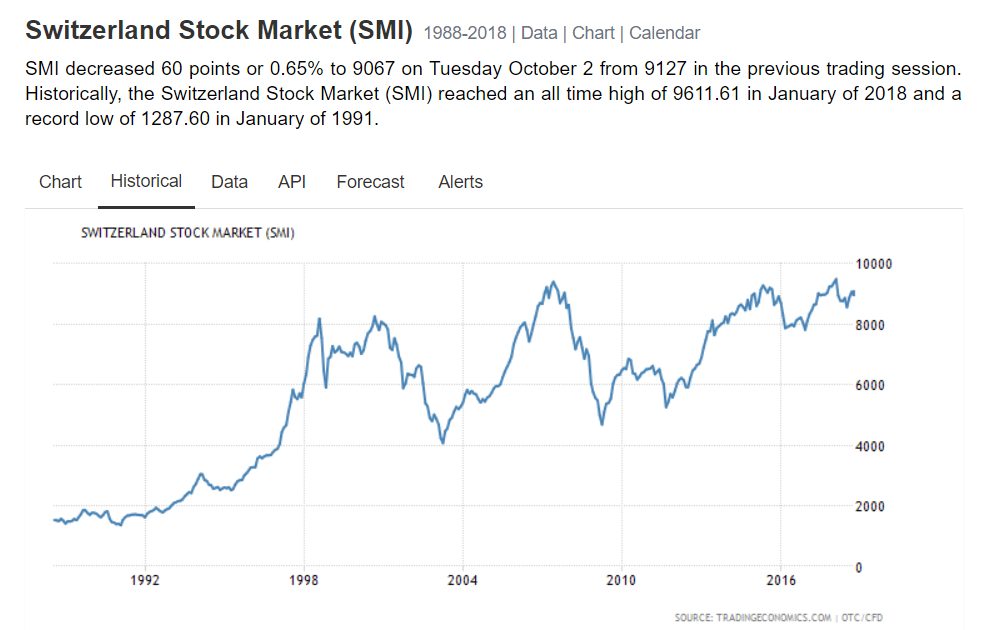

Investing in Swiss stocks

If using one of Switzerland’s EFTs to multiply your capital (investing into ADRs or opting for the most complex way of using one of the 2 stock exchanges direct), Swiss stock is still one of the most trusted options on the investment horizon. Switzerland welcomes domestic and foreign capital alike with foreign direct investment stock in the country amounting to 1 059 777 million USD in 2017.

Useful resources on Stock Investment in Switzerland:

- Investing in Switzerland – brief overview by the balance

- Swiss Index Funds Search by Swisscanto

- SIX Group: Swiss Indices List

Equity Funds Outperformed by Benchmarks, source: AEI

(no data on Switzerland, but no reason to think the result is going to be different)

Switzerland Stock Market Index - probably, the only safe option to invest in Swiss stocks in the long run.

1-year return at the date of writing this article: 1.42% (Bloomberg)

3. Hedge fund investments in Switzerland

Returns: Vary widely, not predictable.

Risks: Highly not recommended, as most funds perform worse than the average market performance in the long run.

As the purpose of this article is mostly to familiarize our readers with how to invest amounts of money below 100K, the hedge funds subtopic is way beyond the point, as it requires larger amounts and has a high threshold to enter in every meaning. For those totally uninitiated, a classic real-life example of hedge funds would be Soros Fund Management by George Soros, and the fictional favorite would be “Axe Capital” in the “Billions” series by Showtime.

Again, statistics suggest that most hedge funds can’t beat the market in the long run. There are a few exceptionally good hedge funds who consistently performed better than the market, like Ray Dalio’s Bridgewater Associates and George Soros’ Fund Management, which stayed profitable during the crisis. 100K is definitely below the radar of these funds, and some of them (like Bridgewater Associates) are closed for new investors and even let go some of their old investors.

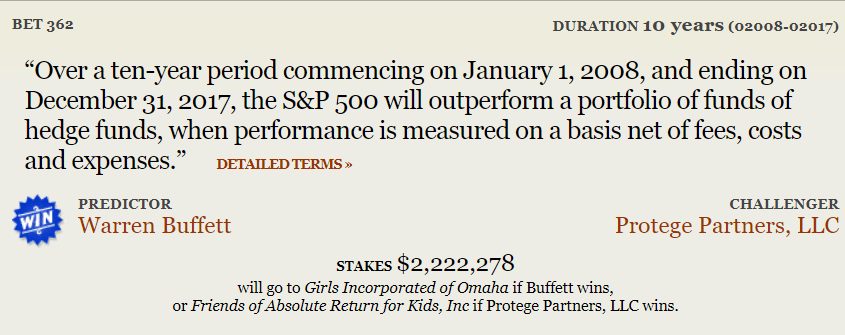

Before investing into a hedge fund (what we wouldn’t recommend), consider the following: in 2008, Warren Buffet issued a challenge, betting $1M that a basket of hedge funds wouldn’t beat S&P 500 in over 10-years. In 2018, he won the bet.

Buffett’s bet against hedge funds: link

4. Direct real estate investments: investing in Swiss property

Returns: From 2% to 4% p.a. for mid-market; 10% and higher for luxury properties.

Risks: The demand can be dependent on nearby factories and offices of big companies.

Real estate investments are considered a cornerstone of building wealth, but when it comes to the Swiss real estate market, the most lucrative deals are closed to investors who can’t put at least a million dollars on the table.

The cost to buy a property or an apartment downtown in a city like Zurich starts from 600K CHF up. From my 20 years experience investing in real estate, I can tell you that the best returns are made on properties in premium locations, where the prices start from 2M – 4M CHF.

You can make double-digit returns if the deal was properly structured and you are skillful enough to manage the property well. There are other models to increase the profit even more, like long-term leasing: owners are often willing to give up to 30% discount if the property is being rented for 20 years, as they can transfer vacancy risk onto the lessee.

Unfortunately, putting a few million into a property is not an option for many. Rates in rural areas and city outskirts are more accessible for beginning investors, but the rental rates are also too low to make this option attractive, considering its risks. Let’s consider this option in detail.

If you have at least 100K to invest into real estate, then you can leverage the money by a 1:4 ratio, so you can buy a 400K property. But even in this case, you will have to buy a property far outside the city center or in a rural area.

In such places, the rental demand for your property will rely greatly on the activity of nearby companies and factories, whose workers can rent your apartment, or immigrants, who oftentimes look for the cheapest rental options.

You don’t bear these risks if you invest in high-end luxury properties in the city center, where there’s always some kind of demand - either through long-term or even short-term rentals. That’s because every solid company looks to provide housing in the most prestigious locations, and you don’t rely on a particular market segment or a specific company.

Let’s look at the economic trends that impact leveraged properties in more detail. Central Bank’s interest rates were less than 0.5% since 2010, and they are negative at the moment. That means that leveraged investments into real estate were attractive for a long time, and many investors already ran this model.

The Central Bank controls the economy by cyclically adjusting the rates, so when the rate goes up, many investors won’t be able to pay the interest and will be forced to sell the property. That means that the prices will fall, as the market will face a liquidity problem – too many people will be selling their properties.

As the valuation of your property falls (which equals the value of your collateral), the bank can demand to review the interest rate accordingly, and if you fail to pay the interest, you will be forced to sell. Consider that in the best case and best time, you will be making 2% – 4% returns p.a., given that you have a 100% occupancy and the interest rate for your loan is below 1%.

Pluses of real estate investment:

- Properties in central areas have a stable, diversified demand.

- You can leverage your money to buy a more expensive property.

Minuses of real estate investment:

- Increased risks when doing a leveraged purchase.

- The market in many regions of Switzerland is considered “heated”.

- Most profitable properties in central areas are not available to an investor that is looking to invest 100K or less.

- Property condition is deteriorating with time, so its value decreases.

- Managing the rent, finding the tenants, and signing contracts is a job in its own right that consumes time and money (escrow, attorney, agent fees, etc.).

Useful resources on Real Estate investment in Switzerland:

- Swiss Real Estate Bubble Index

- Homegate.ch – Real estate portal with an easy search to buy, sell, rent and lend real estate in Switzerland.

- Swiss house prices dynamics explained by Global Property Guide

Some luxury properties, when taken on a long-term lease and rented out on a daily basis (short-term rentals), can make up to 20% returns p.a. on the invested capital

5. Real estate crowd-financing

Returns: 6% to double digits, depending on the model.

Risks: The demand can be dependent on nearby factories and offices of big companies.

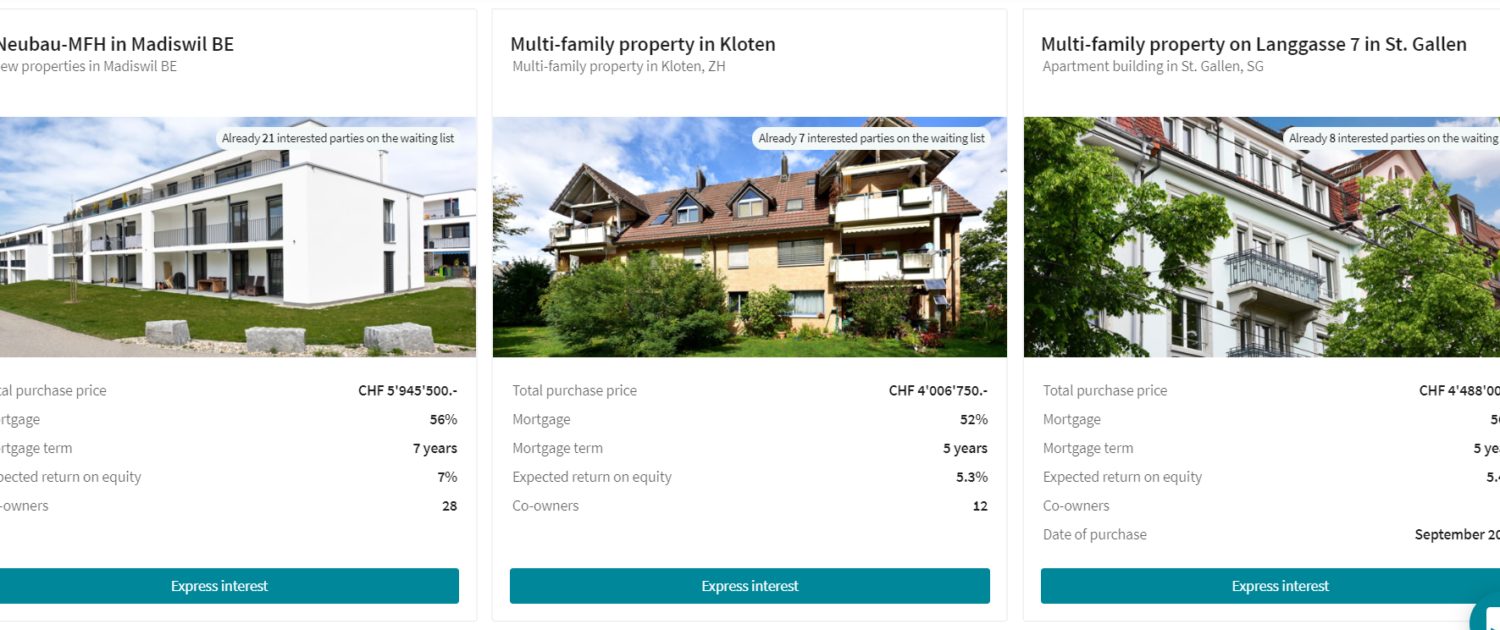

This is one of the very few options for tapping into the game of the Ultra Rich with only a few hundred thousand in the pocket. Real estate crowd-financing helps smaller investors to put their money together and buy a property that no one of them can afford individually.

Among Swiss real estate crowd-financing platforms, Crowdhouse.ch and Foxstone.ch are the most notable; they make investing 100k in real estate with good returns more realistic. The definite leader is the first one on the list and it is highly recommended that you check out Crowdhouse.ch reviews to see for yourself if this is a good choice for your specific investment needs.

The biggest drawback to using Crowdhouse is that they do not invest in luxury housing, instead preferring smaller cities and suburbs. This means that your demand can decrease if the economic situation in the region changes.

For example, if the property is located in a smaller town and the biggest factory fires a significant number of its employees, the tenants can have no funds to pay rent. Office relocations are also happening quite often, causing tenants to leave rentals. Similarly, immigration levels are decreasing, which puts landlords who own budget housing in danger. One month of unpaid rent will likely eat out all the profit.

In contrast, when applied to the luxury property market, the crowd-financing model can drive double-digit returns.

Major pluses of crowd-financing in Swiss real estate:

- Low entrance threshold with some property prices allowing as little as 20K minimum to partake in a crowd-financing of the real estate deal.

- Little involvement after sealing the deal, so your passive income remains passive. For a commission, crowd-financing platforms deal with the day-to-day management of the property.

Main minuses of the Crowd-Financing:

- Rural areas and city outskirts are less attractive as an object of investment, as they rely on fewer sources of demand.

- Some platforms that use leverage (including Crowdhouse.ch) make owners personally liable for the mortgage; this means that if the price of the building drops to the point where the bank will lose its money, the owners will be urged to put up their personal assets to refinance the building.

Useful resources on Crowd-Financing in Switzerland:

Crowdhouse’s expected returns and typical investments

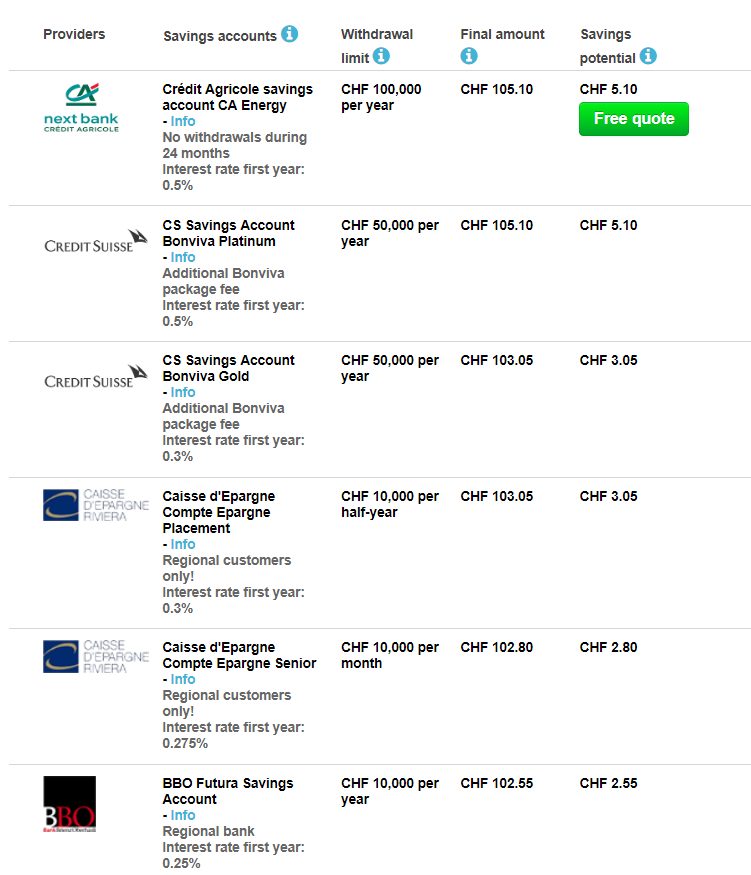

6. Investing money in Swiss banks

Returns: -0.5% to 0.5% p.a.

Risks: There is no collateral that the bank can provide to investors.

Indeed, the Swiss bank system is considered one of the safest and most secure – both in terms of keeping your capital intact as well as keeping your funds away from prying eyes. But if you are looking to multiply or even slightly grow your money – you might be better off looking at another option, as interest rates are far from leading positions in the world, or Europe for that matter.

Be it a savings account, a deposit, or an online trading account – the money is safe indeed, but it sticks to a strict diet, so to say, interest-wise. In recent years, some deposits have even been subject to negative interest rates.

Useful resources on Bank Investments in Switzerland: