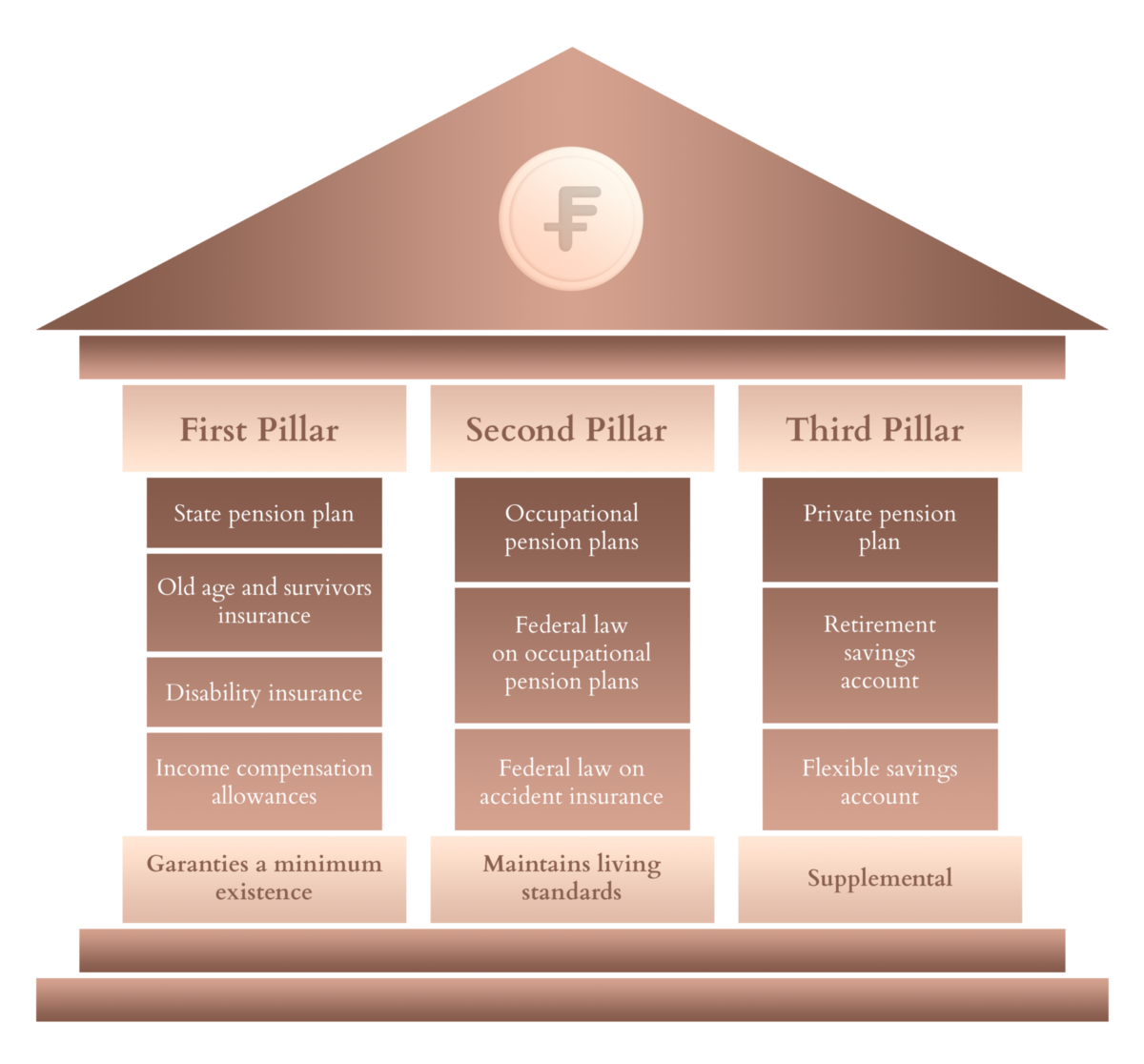

First pillar

Contributions to the first pillar are mandatory for employees or self-employed as of 17-years-old and for everyone regardless of their employment status as soon as they reach the age of 20 until their legal retirement age. It consists mainly of the Old-Age and Survivors Insurance (OASI) and is governmental. The OASI is based on a solidarity concept which means that the current working population pays the contributions which finance the OASI-pension of today’s retirees. Moreover, income from employment is subject to unlimited contributions. This means a redistribution from higher earners to lower earners as the pension paid out is limited to a maximum of СHF 2'390 per month for individuals and СHF 3'585 for married couples. The contributions are paid as a fixed percentage of the salary, half by the employee and half by the employer. Self-employed have to pay the entire contributions themselves.

Second pillar

The core of the second pillar is the occupational pension fund which is mandatory for most employees. It complements the OASI and aims to keep an adequate living standard after retirement. By law, employees earning more than СHF 21'150 per year are automatically insured by an occupational pension fund. In contrast to the first pillar, self-employed people are not forced by law to pay into the pension fund but can choose to do so. Contributions are paid in part by the employee and the employer. The law requires the employer to pay at least half of the contributions, but (s)he can voluntarily pay more.

Like the OASI, the occupational pension fund only ensures a maximum annual salary. Those contributions are invested in low to moderate-risk assets by the pension fund and offer a guaranteed minimum yearly interest rate that is, however, often relatively low.

Unlike the OASI, the money paid into the second pillar can, under certain circumstances, be withdrawn before retirement age which, of course, brings the risk of having too low of a pension when retired. Among those exceptional circumstances are, for instance, if someone wants to buy an owner-occupied residential property, start his own business, or immigrate permanently to a non-EU and non-EFTA country.

On average, the first and second pillars combined should secure a pension of approximately 60% of the income earned before retirement. However, given the high cost of living in Switzerland, this is often not enough to live a comfortable life as a retiree and underlines the importance of additional savings, such as the third pillar.

Third pillar

With the third pillar, employed and self-employed can increase the expected pension through voluntary payments or savings. This reduces the gap between the income earned before retirement and the pension provided by the first and second pillars. Thus, a third pillar solution is vital to keep up with a similar lifestyle once you are retired.

Since the third pillar is a private pension plan, many different options exist. However, generally speaking, one can differentiate between pillar 3a, a restricted private pension plan, and pillar 3b, an unrestricted private pension plan.

Pillar 3a consists of savings one can accumulate during one’s working life until retirement age, either at a bank or with an insurance company that offers some combined insurance benefits. There is an annual maximum amount of contributions paid into a 3a solution. However, those are fully tax-deductible and thus much more attractive than regular savings accounts.

Unlike the first and second pillars, one also has much more control over how the savings are invested - if at all - and thus can potentially earn higher yields. On the other hand, like the second pillar, early withdrawals are only possible under specific circumstances and usually go along with a one-off tax.

Pillar 3b solutions are savings in the form of cash, a saving account, life insurance, or investments. Although there is no limit on annual contributions, there is also no tax deductibility. Despite the lack of tax advantage, 3b solutions have the advantage that they are much more flexible. This means that you can withdraw the capital at any time.

Summary

Retirement provision is undoubtedly a crucial topic. To sum up, the first and second pillars aim to cover the basic living expenses and will make up around 60% of the last salary before retirement. Therefore, it is essential to start thinking about old-age provisions early in life. With its different solutions, the third pillar has precisely this purpose and is vital to living a comfortable life as a retiree without financial worries.