Final thoughts

When entering the stock market battleground, it's wiser to have an army behind you than to go it alone. Investing in a fund via an asset management company could provide you with immense benefits that you can’t necessarily achieve on your own, including financial expertise, scale, and diversification. However, the lack of competitive returns, liquidity, and exorbitant fees can negate nearly all the returns.

In volatile market times, a meager return is still better than none. But, what if you could increase your earnings and simultaneously gain knowledge of investing on your own? The concept of “learning by doing” is an excellent starting point.

One way to achieve this is to leave the majority of your wealth to be managed by the big players, but take a smaller share (at least 10%) to make independent investment decisions, learn more, and potentially increase returns.

Le Bijou can assist in this endeavor. Imagine an ideal scenario: you plan to invest CHF 1 million in an asset management company that yields a 5% annual return. At the end of the year, you earn CHF 1’050’000. While CHF 50’000 is a good return, why settle for good when you can achieve greatness?

By allocating 90% of your assets to a reputable asset management firm and managing the remaining 10% on your own, you can capitalize on exceptional investment opportunities, such as the Le Bijou Bahnhofstrasse 89 project in Zurich, which boasts a remarkable 22.22% annualized return. This strategic approach could result in a staggering CHF 1’067’000 return, a remarkable 34% increase.

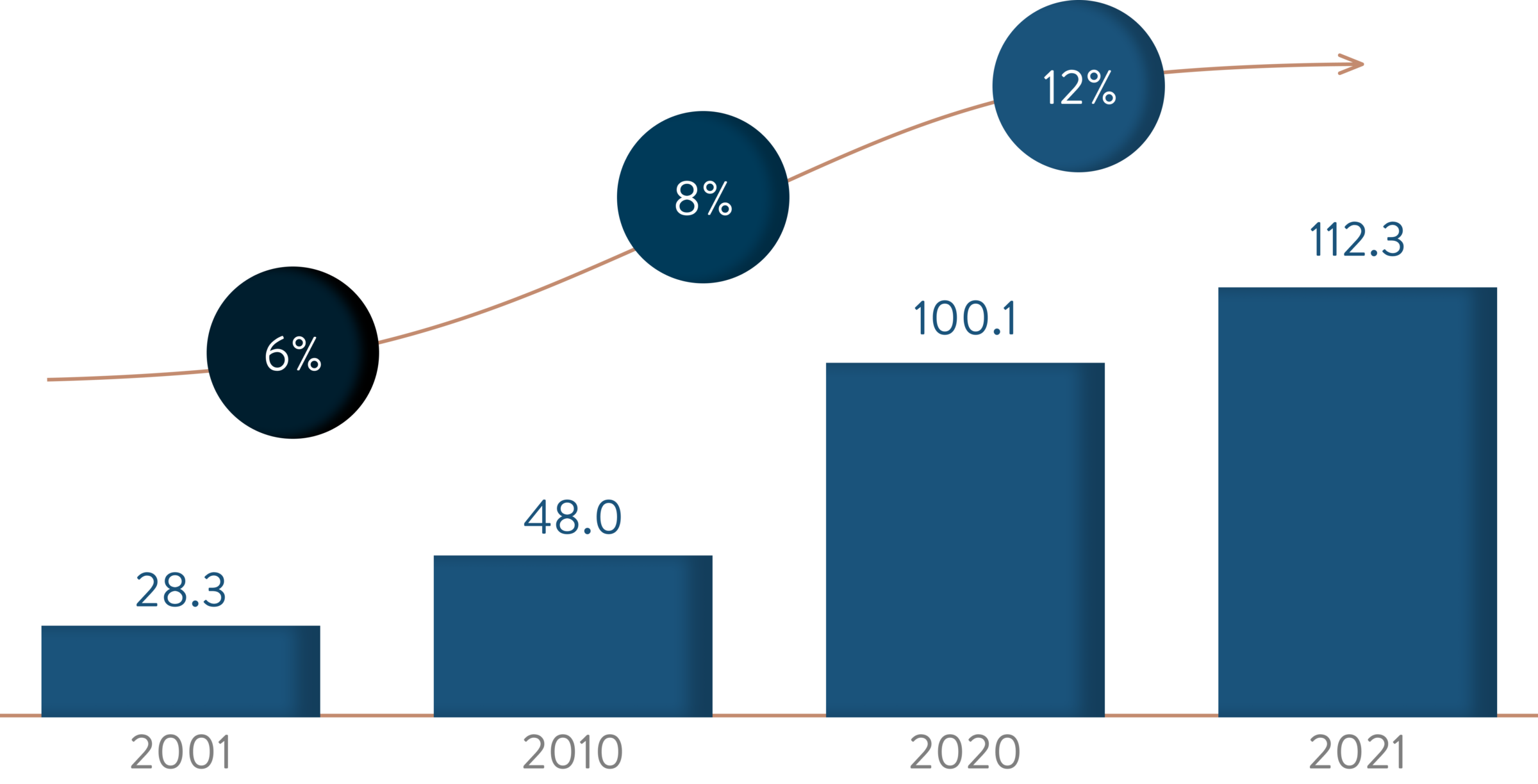

Furthermore, you can harness the power of compound interest and reap impressive investment returns. In over a decade, your initial investment could grow to nearly CHF 1.6 million, but by taking the latter approach, you could achieve over CHF 2 million, a potential increase of 29.23%.

While relying on professional managers may provide a sense of reassurance, it does not guarantee personal growth. True knowledge is something only acquired through practical experience.

“The best way to learn is by doing; never ask others to do what you’re not willing to do yourself.” — Ellen Sauerbrey